Market Trends: Beef in USA

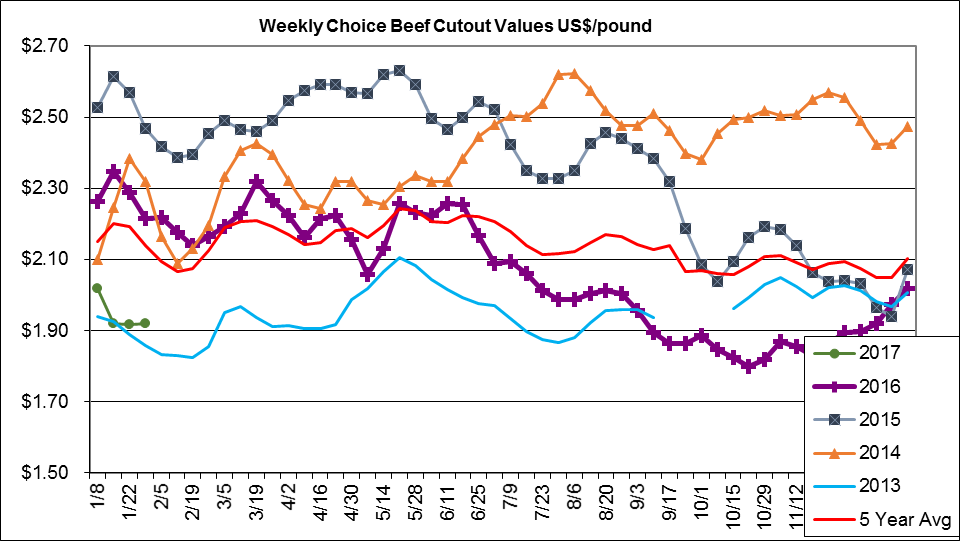

The Choice cutout trended higher through the end of the year before dipping to $1.92/lb. in the second week of January. The cutout was still $1.92/lb. for the week ending January 27, down 13% from 2016 and down 11% from the previous 5-year average. The Choice/Select spread was $3.52/cwt. For the month of January, the cutout was at similar levels to 2012 and 2013 prices. All Choice primals were down year-over-year for the week ending January 27: short plates ($1.21/lb., -5%), ribs ($2.92, -8%), flanks ($1.02, -9%), loins ($2.51, -11%), rounds ($1.74, -16%), briskets ($1.42, -16%),, and chucks ($1.61, -18%).

The chuck primal decreased through the month of January, and so far in 2017, the chuck primal has had the worst primal performance compared to year-ago prices. The ribs and loin primals trended seasonally higher for the end of the year holidays, but items like ribeyes and tenderloins have come down from their December highs and are now below prices for the last few years.

For the week ending January 27, prices were lower year-over-year for top butts ($2.38, -21%), ribeyes ($6.16, -12%), tenderloins ($9.04, -9%), and ball tips ($2.27, -8%), while values were higher for tri-tips ($3.91, +9%) and NY strips ($5.54, +1%). Briskets (deckle-off bnls) were lower year-over-year at $2.07, -21% along with petite tender ($3.60, -20%), flank steaks at ($4.30, -17%), and top blade (flat iron) ($2.71, -13%).

Prices were down for other top export items including rib short ribs ($4.00, -10%), chuck short ribs ($3.07, -1%), chuck rolls ($2.56, -10%), chuck shoulder clods ($1.90, -19%), and top inside rounds ($1.97, -14%).

USDA estimates that 2016 beef production was up 6.4% from 2015 at 11.44 million metric tons (25.2 billion pounds). 2017 production is expected to increase by another 2.9% to 11.77 million metric tons (26.0 billion pounds) which would be the largest since 2011.

Source: USMEF