Market trends: Beef

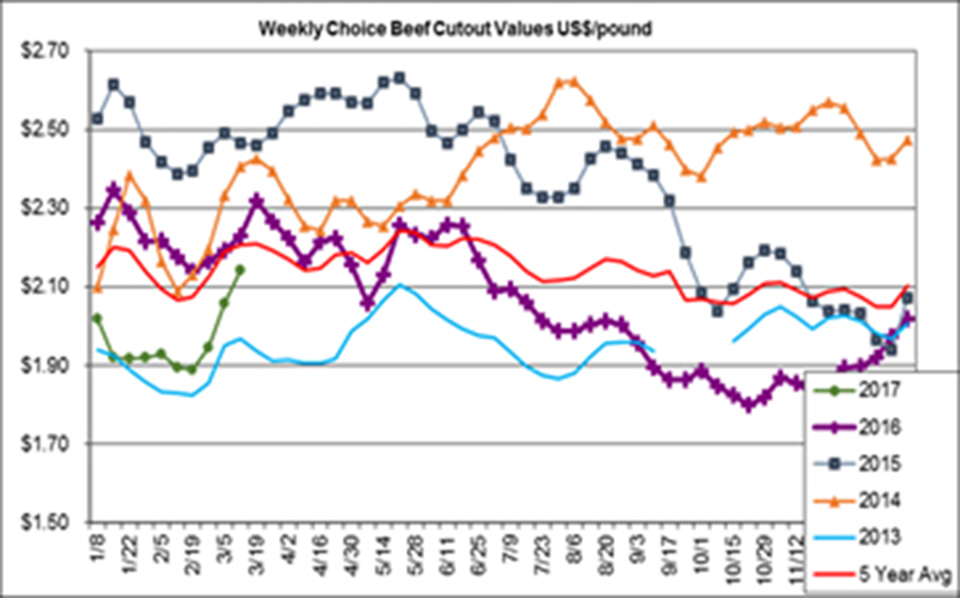

The Choice cutout had large value increases in Mar as seasonally higher values for ribs & loins pushed the cutout higher. However, on Mar 10, the Choice cutout was $2.14/lb., down 4% from 2016 and still at the lowest level since 2013, for this time of yr, reflecting larger production. The Choice/Select spread was $0.07/lb. Choice short plates ($1.53, +3%) and rounds ($1.81, +1%) were higher yr-over-yr, while values were lower for ribs ($3.18, -13%), flanks ($1.24, -6%), briskets ($1.50, -6%), loins ($3.11, -4%), & chucks ($1.65, -1%). Loin & rib values have increased a lot since the end of Feb: the loin increased from $2.63/lb. to $3.11/lb., and ribs from $2.88/lb. to $3.18/lb., although both remain below last yr’s values. For the wk ending Mar 10, prices were lower for ribeyes ($6.91, -17%), top butts ($3.33, -13%), briskets (deckle-off bnls) ($2.13, -14%), flank steaks ($5.23, -12%), top blades (flat iron) ($2.71, -8%), & tenderloins ($10.57, -2%); even for ball tips ($3.14), petite tenders ($4.82) & NY strips ($7.06); and higher for tri-tips ($4.03, +10%).

Exports continue to exceed yr-ago levels with higher prices for popular cuts: rib short ribs ($4.35, +5%), chuck short ribs ($3.17, +19%), top/inside rounds ($2.48, +10%), & chuck shoulder clods ($1.98, +1%); and lower for chuck rolls ($2.30, -14%). USDA estimates that 2016 beef production was up 6.4% from 2015 at 11.44 mill MT (25.2 bill lbs). 2017 production is expected to increase by another 4.1% to 11.91 mill MT (26.25 bill lbs) which would be the largest since 2010.